Onboarding as a growth channel

Hayyak, a digital account opening journey for a UAE retail bank.

Onboarding is the most expensive screen in a bank. You pay to acquire the customer, then you risk losing them inside the very flow that is supposed to welcome them. This UAE retail bank was doing exactly that, every day. The fix was not a faster KYC. It was deciding that onboarding was a product, not a compliance flow.

The brief

The bank had a four-day branch-led onboarding journey and a digital path that loaded customers into the same compliance form, only smaller. The brief asked for a faster KYC. The work re-framed the brief: design onboarding as a product, with acquisition, activation, and cross-sell as first-class outcomes alongside the regulatory ones.

The problem, defined

Acquisition cost was rising. Completion was falling. Cross-sell ran on a follow-up campaign customers rarely opened. Compliance saw onboarding as a regulatory checkpoint. The business saw it as a leaky funnel. Both were right, and neither was designing for the other.

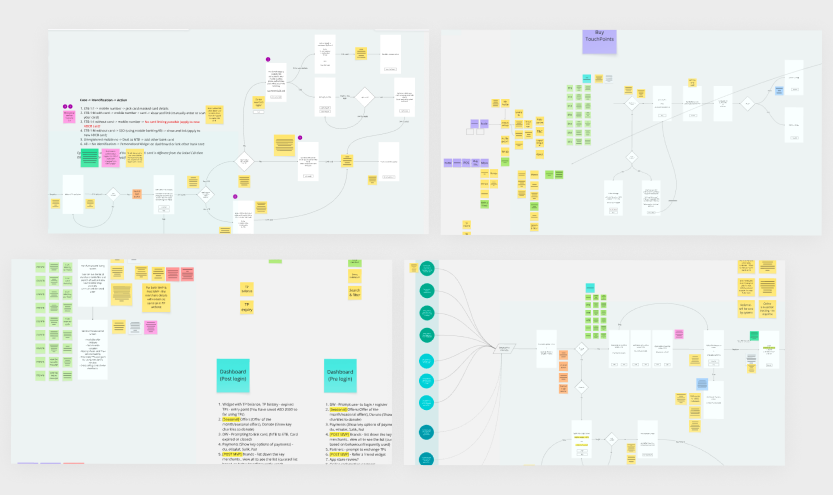

From workshop to flow

We ran a multi-day workshop with the bank's product, risk, ops, and compliance leads. The output was a wall of requirements, decision points, and edge cases across four streams, identification, touchpoints, dashboard pre-login, dashboard post-login. I translated the wall into a single high-level flow, not as a clean-up exercise but as a contract. Anything not on the flow did not get built. Anything on the flow had a named owner.

The tradeoff that shaped the design

Compliance density against flow speed. Risk wanted to front-load every disclosure. Acquisition wanted to defer everything possible. We split the difference with progressive disclosure. Regulatory steps stayed mandatory but were sequenced to follow declared customer intent, not the bank's internal taxonomy.

What I designed

- A service blueprint across compliance, KYC, and core banking. It surfaced which "requirements" were regulatory and which were institutional habit. The second list got shorter quickly.

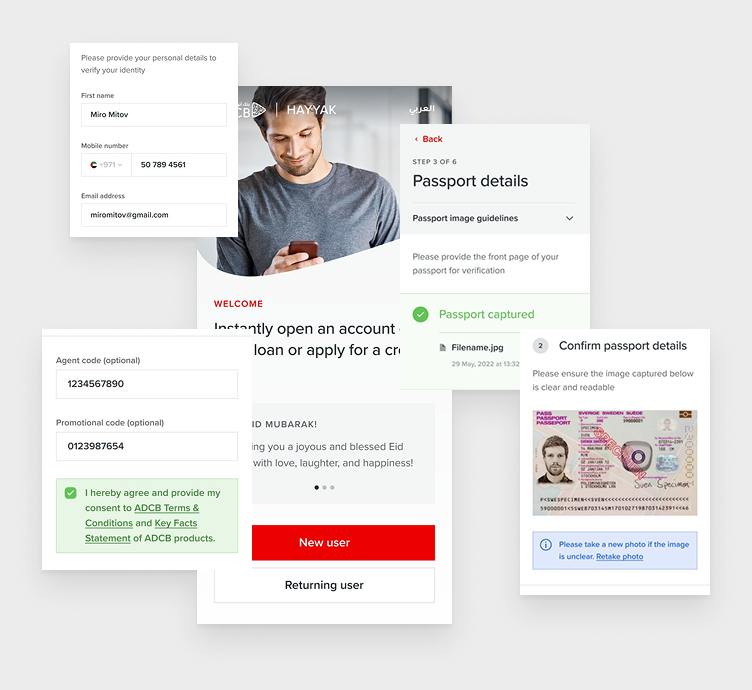

- An in-app capture flow for passport, ID, and biometrics with OCR and automated verification, plus a clear retake path when the capture failed quality checks.

- An agent-assisted path for higher-touch customers, sharing the same backend with a dense, code-driven UI. One source of truth, two surfaces.

- Bundled product offers inside onboarding at the moment of decision, not as a post-completion email. Cross-sell became a step, not a campaign.

- Bilingual support in English and Arabic with full RTL behaviour, not translation alone.

Outcomes

- Onboarding time compressed from days to under ten minutes on the digital path.

- Cross-sell attach rate on credit card products lifted by an estimated 12 to 18%.

- Branch onboarding load reduced for the digital cohort.

- Customer acquisition cost trended down on the digital channel.

Caveat: directional figures based on internal benchmarks; exact numbers under NDA.

The lesson that outlasted the launch

Onboarding is not a compliance flow. It is the first product. Treating it as a growth surface changed which features won the prioritisation argument, not just which copy got approved.